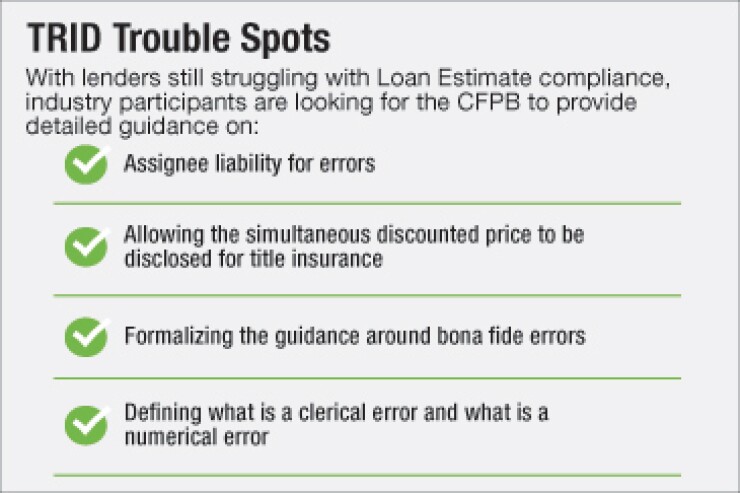

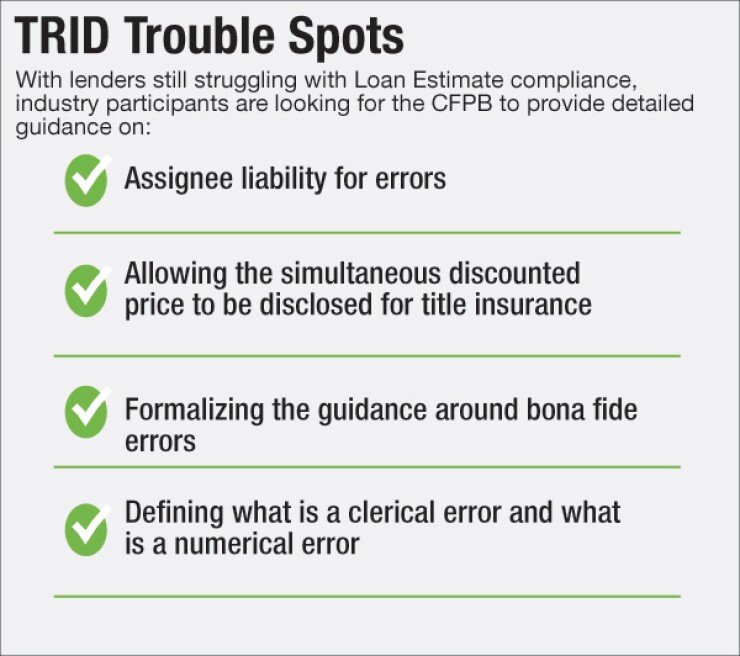

Secondary market loan purchaser liability is probably the juiciest topic that the Consumer Financial Protection Bureau will address in its expected clarifications of TILA/RESPA integrated disclosure rules in July.

While most of the assignee liability risk is associated with the Closing Disclosure — the required form provided to consumers prior to closing to help them understand their transaction costs — the issue even affects the Loan Estimate form, which informs consumers about the key features, costs and risks of the mortgage they are applying for. Loan purchasers have discounted and even

Secondary market liability has been a frequent subject of informal guidance from the CFPB on the Truth in Lending Act and Real Estate Settlement Procedures Act integrated disclosures, also known as TRID, including a mention by Richard Cordray, bureau director, in a December letter.

Without formal guidance on the liability issue, people in the mortgage industry are afraid to rely on those CFPB statements. "I think that probably the biggest and best thing that could come out of this proposal, hopefully, is for the CFPB to officially endorse those policy statements that they have already made and hopefully make people a little less worried in the secondary market," Cremata said.

As the industry has gotten used to working under TRID, fewer loans are being rejected by the secondary market for LE errors; most rejected loans are because of issues with the Closing Disclosure.

But some investors are taking a very conservative approach, purchasing a loan at a discount or declining to purchase it at all if the LE is wrong, even if it is corrected on the CD, said Donna Clayton, chief compliance officer for LenderLive Network.

Based on Cordray's December letter, Clayton said the CFPB will likely determine that if the final CD is correct, the lender or creditor will not be liable for an error on the initial LE. The bureau is also likely to define what is considered a clerical error, which is typically not a concern for secondary buyers, versus what is a numerical error, which can be a concern.

However, Clayton said, "The CFPB doesn't want the mortgage lenders to go back and not really pay attention to these LEs; they still want you to make a good-faith effort that they're accurate."

The CFPB has said informally that a particular provision in the Truth-in-Lending Act — one that does not hold lenders or investors liable for a violation when it is an unintentional, good-faith error — should apply to TRID errors, and that position could be formalized in the July guidance, said Grant Bailey, managing director at Fitch Ratings.

"That's part of the ambiguity, that it's unclear what carries through from TILA and what carries through from RESPA. So I think providing some of that clarity is what they're going to focus on," Bailey said.

Technology vendors are also looking for more clarity from the CFPB. John Vong, president of ComplianceEase, said he hopes the CFPB's July clarifications will help both lenders and technology providers clean up some of the uncertainty that has developed.

"We have due diligence customers and they get feedback that some provider might not have captured these kinds of data, the other tech provider will capture other data," Vong said. "Further clarification from the bureau will give everyone a better understanding so that we are all on the same page."

Another potential area to be addressed is how to treat what the industry refers to as the "simultaneous discount" for title insurance, Clayton said. The simultaneous discount refers to the discounted premium that is provided when an owner's title policy, which is optional, and a lender's title policy are both purchased.

Currently, the TRID rules don't allow for disclosure of the simultaneous discount on the LE, so the actual amount the borrower will have to pay at closing is overstated, Clayton said.

This is an issue that the American Land Title Association has been active on since the TRID rule became effective in 2014. ALTA just circulated a letter in June signed by members of the U.S. House of Representatives from both parties, asking that the simultaneous issue

On the other hand, even if the CFPB were to formalize some of its positions, courts could apply different interpretations in private liability and class action lawsuits, Cremata said.

"I am curious to see whether even this will be enough for secondary investors, but I think it will definitely go a long way," he said. And ironically, giving more definitive directions to the market could end up giving the CFPB a stronger position if it decides to take enforcement action.